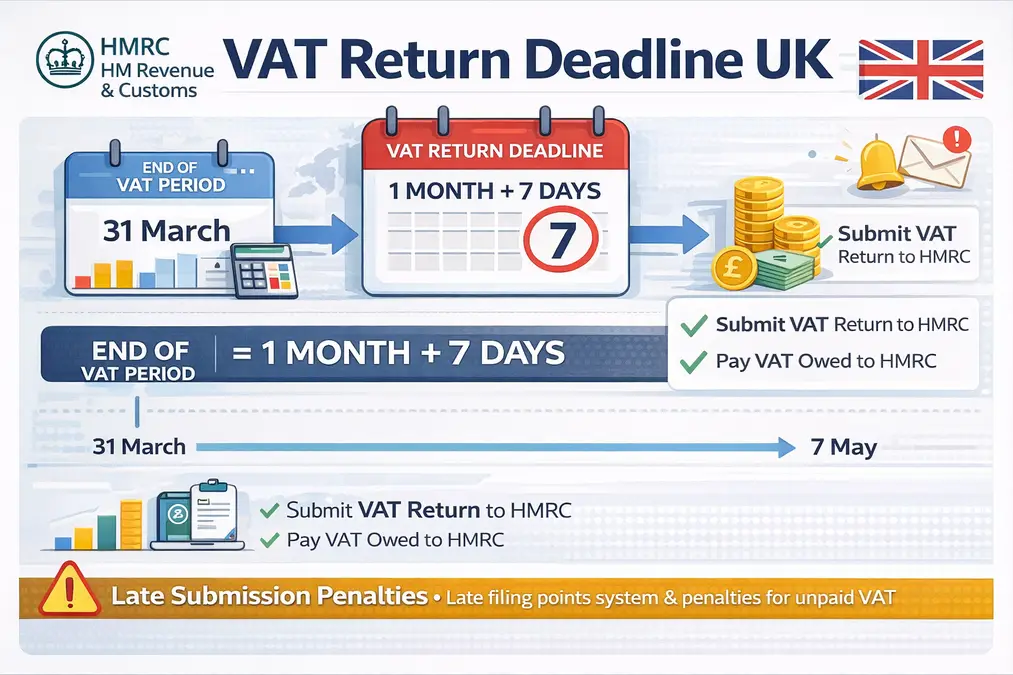

The VAT return deadline UK determines when VAT-registered businesses must submit their VAT return and pay any VAT owed to HMRC. According to HM Revenue & Customs, most VAT returns must be filed one calendar month plus seven days after the end of the VAT accounting period.

Understanding the VAT return deadline UK is essential for maintaining compliance, avoiding penalties, and ensuring accurate VAT accounting under Making Tax Digital (MTD) rules.

This guide explains the official deadlines, filing schedules, payment timelines, reverse charge considerations, and common compliance risks.

- What Is the VAT Return Deadline UK?

- VAT Accounting Periods in the UK

- Filing VAT Returns Under Making Tax Digital (MTD)

- What Information Is Included in a VAT Return?

- Domestic VAT vs Cross-Border Transactions

- What Happens If You Miss the VAT Return Deadline UK?

- How to Submit a VAT Return Before the Deadline

- Common VAT Return Errors

- Compliance Checks and HMRC Investigations

- Frequently Asked Questions

- Conclusion

What Is the VAT Return Deadline UK?

The VAT return deadline UK is the date by which a business must:

- Submit its VAT return to HMRC

- Pay any VAT owed

For most businesses:

Deadline = End of VAT period + 1 month + 7 days

Example:

| VAT Period End | VAT Return Deadline |

|---|---|

| 31 March | 7 May |

| 30 June | 7 August |

| 30 September | 7 November |

| 31 December | 7 February |

Businesses should calculate VAT correctly before submitting returns. Our guide on UK VAT calculation explains the formula used in VAT returns.

VAT Accounting Periods in the UK

Most businesses submit quarterly VAT returns.

Typical quarterly periods include:

- January – March

- April – June

- July – September

- October – December

However, some businesses may use:

Monthly VAT Returns

Often used by businesses regularly claiming VAT refunds.

Annual Accounting Scheme

Businesses submit one VAT return per year with advance payments during the year.

More details are explained in our guide to UK VAT accounting schemes.

Filing VAT Returns Under Making Tax Digital (MTD)

Since April 2022, all VAT-registered businesses must follow Making Tax Digital (MTD) rules.

This means:

- VAT returns must be submitted using MTD-compatible software

- Records must be kept digitally

- Manual entry through the Government Gateway is generally no longer allowed

MTD compliance does not change the VAT return deadline UK, but it changes how returns must be submitted.

What Information Is Included in a VAT Return?

A VAT return normally includes the following figures:

- Total sales and output VAT

- Total purchases and input VAT

- VAT owed to HMRC

- VAT reclaimable

- Net VAT payable or refundable

Understanding net vs gross pricing is essential for accurate reporting. Our guide to net vs gross price with VAT explains how these values appear on invoices.

Domestic VAT vs Cross-Border Transactions

Businesses must consider special VAT rules before submitting a return.

Domestic Supplies

VAT must be charged according to official UK rates:

- Standard rate: 20%

- Reduced rate: 5%

- Zero rate: 0%

You can read a detailed breakdown in UK VAT rates explained.

Zero-Rated vs Exempt Supplies

Understanding this distinction affects VAT returns.

Zero-rated supplies

- VAT rate = 0%

- Still reported on VAT return

- Input VAT recoverable

Exempt supplies

- No VAT charged

- Input VAT normally not recoverable

Reverse Charge Mechanism

The reverse charge applies when:

- UK businesses receive services from overseas suppliers

- Certain domestic construction services are supplied

Under reverse charge rules:

- The customer reports VAT instead of the supplier

- VAT is recorded as both output VAT and input VAT on the VAT return

What Happens If You Miss the VAT Return Deadline UK?

Missing the VAT return deadline UK can lead to penalties.

HMRC operates a points-based penalty system for late submissions.

Late Submission

Penalty points are issued each time a VAT return is late.

Once the threshold is reached, a £200 penalty applies.

Late Payment

Separate penalties apply for unpaid VAT:

- No penalty if paid within 15 days

- 2% penalty after 15 days

- Additional 2% after 30 days

- Daily interest charges may apply

How to Submit a VAT Return Before the Deadline

To meet the VAT return deadline UK:

- Maintain digital VAT records

- Use MTD-compatible accounting software

- Calculate output and input VAT

- Submit VAT return electronically

- Pay VAT owed using HMRC approved payment methods

Businesses often verify calculations using tools like the UK VAT calculator.

Common VAT Return Errors

According to HMRC compliance checks, common mistakes include:

- Incorrect VAT rates

- Misclassifying zero-rated and exempt supplies

- Reverse charge accounting errors

- Claiming input VAT on ineligible purchases

- Submitting returns after the VAT return deadline UK

More examples are explained in common UK VAT mistakes.

Compliance Checks and HMRC Investigations

HMRC may conduct VAT compliance checks when businesses:

- Repeatedly miss deadlines

- Report unusually high VAT refunds

- Show inconsistent turnover figures

- Have errors in reverse charge accounting

Maintaining accurate digital records helps reduce risk.

Frequently Asked Questions

What is the standard VAT return deadline UK?

Most VAT returns must be submitted one month and seven days after the end of the VAT period.

Can I submit my VAT return early?

Yes. Businesses can submit VAT returns at any time before the VAT return deadline UK.

What if I cannot pay VAT on time?

You may request a Time to Pay arrangement from HMRC.

Approval depends on your compliance history.

Do zero-rated sales affect VAT return deadlines?

No. They still must be reported but do not generate VAT payable.

Are VAT return deadlines different for annual accounting?

Yes. Businesses on the Annual Accounting Scheme submit one return per year with interim payments.

Conclusion

Understanding the VAT return deadline UK is essential for staying compliant with HMRC regulations. Most businesses must submit VAT returns one month and seven days after the end of the VAT period, using Making Tax Digital-compatible software.

Accurate reporting of output VAT, input VAT, reverse charge transactions, and zero-rated supplies ensures your VAT returns remain compliant and avoids penalties.

By monitoring deadlines, maintaining digital records, and submitting returns early, businesses can stay fully compliant with HMRC requirements.