Understanding VAT after discount UK is important for businesses offering price reductions, promotional discounts, or trade discounts. According to HM Revenue & Customs, VAT is normally calculated on the actual amount paid by the customer after the discount is applied, provided the discount reduces the selling price.

Correctly applying VAT after discounts ensures that invoices, VAT returns, and accounting records remain compliant with HMRC VAT legislation.

This guide explains how VAT works with discounts, including trade discounts, promotional discounts, conditional discounts, and cross-border considerations.

- What Is VAT After Discount UK?

- Why VAT Is Calculated After Discounts

- Types of Discounts and Their VAT Treatment

- VAT After Discount vs VAT Inclusive Pricing

- Invoice Requirements When Discounts Apply

- Cross-Border Transactions and Discounts

- VAT After Discount and Making Tax Digital

- Common VAT Errors With Discounts

- Best Practices for VAT After Discount Compliance

- Frequently Asked Questions

- Conclusion

What Is VAT After Discount UK?

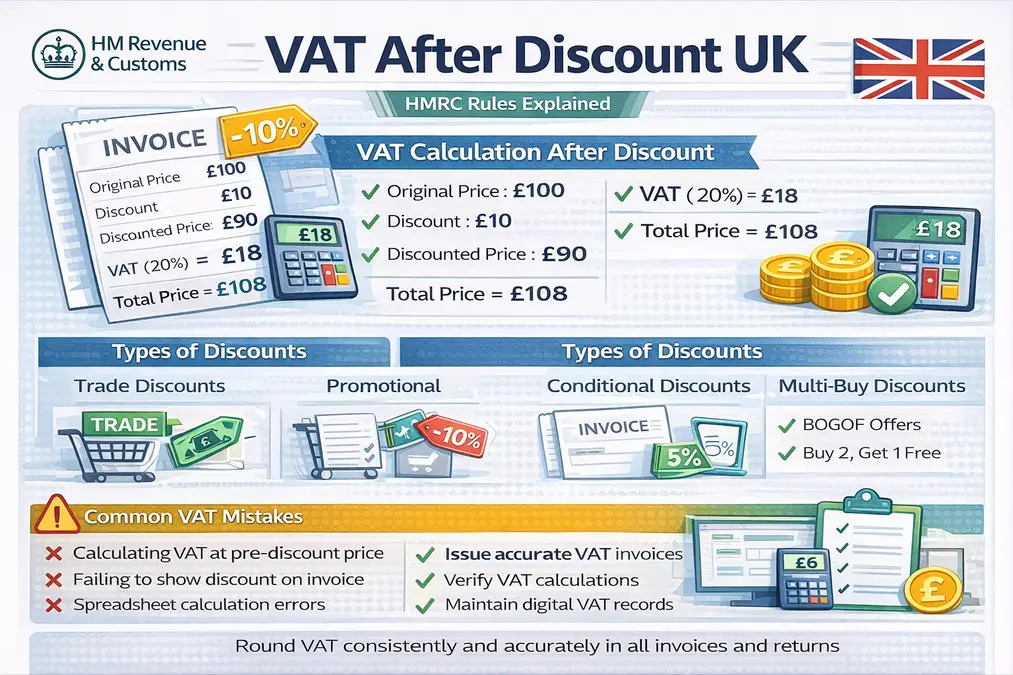

The VAT after discount UK rule states that when a business offers a discount that reduces the selling price, VAT should normally be calculated on the discounted price rather than the original price.

Example:

Original price: £100

Discount: £10

Discounted price: £90

VAT (20%) = £18

Total price payable = £108

Why VAT Is Calculated After Discounts

VAT is a tax on the value of goods or services supplied. When a discount reduces the price paid by the customer, the taxable value decreases.

This means:

Taxable amount = price actually charged to the customer

Understanding how VAT is calculated before and after discounts is explained in our guide on the VAT calculation formula.

Types of Discounts and Their VAT Treatment

Different types of discounts can affect VAT calculations in different ways.

1. Trade Discounts

Trade discounts are reductions offered to customers before the sale is completed.

Example:

List price: £200

Trade discount: 20%

Discounted price = £160

VAT (20%) = £32

VAT is calculated on £160, not £200.

2. Promotional Discounts

Retail promotions such as:

- Seasonal sales

- Percentage discounts

- Coupon discounts

reduce the selling price.

Example:

Original price: £50

Promotion: 10% off

New price = £45

VAT = £9

VAT is charged on the reduced price.

3. Prompt Payment Discounts

Prompt payment discounts encourage customers to pay invoices early.

Example:

Invoice price: £100

Prompt payment discount: 5%

If the customer pays early:

Price = £95

VAT = £19

However, VAT treatment may depend on whether the discount is conditional.

4. Multi-Buy Discounts

Offers such as:

- Buy one get one free

- Buy two get one free

must still allocate VAT correctly across items.

Example:

2 items sold for £10 instead of £12.

VAT applies to the total selling price (£10).

VAT After Discount vs VAT Inclusive Pricing

If prices include VAT, the calculation must be reversed.

Example:

Discounted price including VAT = £96

VAT = £96 × (20 ÷ 120)

VAT = £16

Net price = £80

For more detail, see our guide on removing VAT from price.

Invoice Requirements When Discounts Apply

HMRC requires VAT invoices to show:

- Original price

- Discount applied (if relevant)

- Net amount after discount

- VAT charged

- Total payable

Understanding invoice structure helps businesses distinguish between VAT inclusive vs exclusive pricing.

Cross-Border Transactions and Discounts

Discounts also affect VAT treatment in international transactions.

Reverse Charge

When reverse charge applies:

- VAT is accounted for by the customer

- VAT is calculated on the discounted value of the supply

Zero-Rated Supplies

Zero-rated supplies:

- VAT rate = 0%

- Discounts do not affect VAT liability

However, the value must still be reported on the VAT return.

VAT After Discount and Making Tax Digital

Under Making Tax Digital (MTD), businesses must maintain digital VAT records including:

- Discounts applied

- Net taxable value

- VAT amounts

Accounting software usually calculates VAT automatically after discounts.

Common VAT Errors With Discounts

HMRC compliance checks frequently identify errors involving discounts such as:

- Calculating VAT on the original price instead of discounted price

- Incorrect invoice presentation

- Spreadsheet calculation mistakes

- Misreporting promotional discounts

More examples can be found in VAT calculation mistakes.

Best Practices for VAT After Discount Compliance

Businesses should follow these practices:

- Apply discounts before calculating VAT

- Record discounts clearly on invoices

- Use consistent accounting methods

- Verify VAT calculations before filing returns

- Maintain digital VAT records under MTD

Many businesses verify their calculations using tools like the UK VAT calculator.

Frequently Asked Questions

Is VAT calculated before or after discount in the UK?

VAT is normally calculated after the discount, meaning it applies to the discounted price.

Do discounts reduce VAT payable?

Yes. Because VAT is calculated on the reduced selling price, discounts lower the VAT amount charged.

Does VAT apply to promotional discounts?

Yes. VAT is calculated on the final price after promotional discounts are applied.

Do trade discounts affect VAT invoices?

Yes. VAT invoices should show the discounted price and VAT charged on that amount.

Are multi-buy offers treated as discounts for VAT?

Yes. VAT applies to the actual total price paid by the customer.

Conclusion

Understanding VAT after discount UK is essential for accurate VAT calculations and HMRC compliance. When discounts reduce the selling price, VAT must normally be calculated on the discounted amount rather than the original price.

Correct handling of trade discounts, promotional offers, and conditional discounts ensures invoices remain accurate and VAT returns are compliant with HMRC regulations.